In the News

Exclusive Interview with Anup Maheshwari, Co-founder & CIO, 360 ONE Asset

1. Where do you see markets by FY24?

Having spent more than twenty-five years in the listed equity space, one thing I have absolute certainty about is the inability to have absolute certainty on what the market may be up to in a single day, month or year. One year is too small a time frame to get an estimate of what the market return may look like. Take a look at the image below.

Relation between time volatility and return – Source Bloomberg. The above chart shows the rolling 1yr, 2yr, 3yr, 5yr, 7yr and 10yr returns for Sensex and the volatility in these returns. Volatility has been calculated as the Standard deviation of these returns (dispersion from the mean returns). Data from Jan 2, 1990, to Nov 30, 2022, has been used for this exhibit

The blue line highlights Sensex’s rolling returns from 1990-2022. The green line highlights Sensex’s rolling standard deviation during the same period. As you can see it takes around five years for the return to be higher than the risk and so whenever one is investing in equities, at the very least, one would want to have a five-year investment horizon.

2. What are the three major Headwinds & Tailwinds for the global economy & markets currently?

Headwinds

Rising inflation coupled with rising interest rates impact both businesses and valuations and hence can increase uncertainty in the market. My larger concern though is around the market reaching valuations where the risk-reward may seem less than optimal.

Tailwinds

As companies diversify their supply chain, India is emerging as an attractive option to set camp. Manufacturing exports is a theme which we at 360 ONE Asset (earlier known as IIFL AMC) see as a theme that may play out in India for the next decade.

3. What is your outlook on the Financials, Manufacturing, and Auto Sector?

I remain positive on financials in the long term. Corporate Balance sheets look healthy and retail and corporate sectors should continue to experience reasonable growth.

As I touched on earlier, manufacturing is a trend that may acquire more strength over time given the external factors coupled with the comparative tax environment. India could emerge as a global manufacturing hub over the coming decade.

The Auto sector tends to be quite cyclical. It has performed well over the last year and so my only concern is around the fact that a lot of the upside may already be priced in.

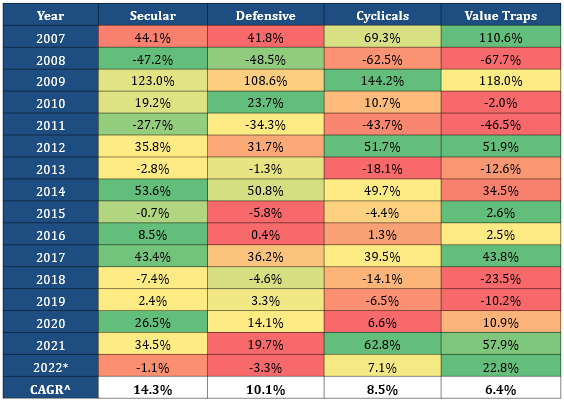

4. What’s your conviction on the SCDV framework for the current decade?

In 360 ONE Asset's SCDV Framework, businesses with a consistently high return on Equity and profit growth show up as secular stocks. In our framework, out of the past 10 years, these businesses need to show a Return on Equity and profit growth greater than 15% for at least 6 years to be classified as secular. Compared to the market benchmark we tend to be overweight on secular businesses.

Defensive stocks are efficient but do not show rapid profit growth that secular stocks do. Cyclicals on the other hand can rapidly grow profits for a few years but may not be very efficient across the cycle. Our portfolio allocation to cyclical and defensive stocks is a function of the prevailing market conditions and economic cycle. Value Traps are businesses that have not demonstrated high growth or efficiency in the past. We usually remain underweight on Value Traps compared to the benchmark.

Source: Internal, Bloomberg, Returns of equal-weighted baskets during calendar years for S&P BSE 200 Index. *Data as on Nov 30, 2022. ^CAGR is for the period Dec 31, 2006, to Dec 31, 2021. Past Performance may or may not be sustained in future.

As the image above shows, in equal-weighted portfolios across these quadrants over sixteen years, seculars are the best-performing quadrant followed by defensives and cyclicals. Value Traps over that same period have delivered the lowest returns. We continue to believe that this will carry on.

While Seculars may have underperformed value traps in the last two years, we are not too concerned, as in the long run we believe that businesses that demonstrate high growth and profitability will do better than the rest. To draw a cricket parallel if a full toss gets you a wicket, you don’t start bowling full tosses every ball. That is not to say that we do not examine businesses that have the potential to switch quadrants. However, we do not feel compelled to make any changes to our SCDV framework.

Talent

Looking for the agility of a start-up and the gold standards of an established financial institution? 360 ONE Asset is the perfect sweet spot for you.